If you’ve ever wondered why a dollar today is worth more than a dollar tomorrow, you’re already thinking about one of the most important principles in finance: time value of money explained in practical, real-world terms. Whether you’re building long-term wealth, evaluating investments, or simply trying to make smarter financial decisions, understanding this concept is essential.

Most people hear the phrase but never fully grasp how it impacts their savings, debt, and portfolio growth. This article breaks it down clearly—without jargon—so you can see exactly how time, interest, inflation, and opportunity cost shape your financial outcomes.

We draw on established financial research, proven capital allocation strategies, and real-world portfolio management insights to ensure the guidance here is both accurate and actionable. By the end, you’ll understand not just the theory, but how to apply it immediately to grow and protect your wealth.

Why a Dollar Today Changes Everything

Would you rather have $1,000 today or $1,000 a year from now? Seems obvious, right? But have you ever wondered why? That simple choice reveals a financial superpower most people overlook. Money today can be invested, earn interest, or seize opportunity. Meanwhile, waiting costs you growth (and patience).

This is the time value of money explained in plain terms: a dollar now is worth more than a dollar later because it can grow. So before you delay investing or savings, ask yourself—what could that money become if you started today? The clock is always ticking.

The Twin Engines of Value: Opportunity Cost and Inflation

Why is a dollar today worth more than a dollar tomorrow? The answer comes down to opportunity cost and inflation—the twin engines behind the time value of money explained in the section.

Opportunity cost means choosing one option means giving up another. When it comes to money, receiving cash today gives you the opportunity to invest it and earn returns. For example, if you invest $1,000 at a 5% annual return, you’ll have $1,050 in one year. That extra $50 isn’t magic—it’s the reward for putting your money to work. If you delay receiving that $1,000, you forfeit the potential gain. (Money sitting idle is like a treadmill—you’re moving, but going nowhere.)

Now meet the quieter force: inflation. Inflation is the gradual rise in prices over time, which erodes purchasing power. If a cup of coffee costs $3 today and rises to $3.30 in a few years, the same dollar buys less. According to the U.S. Bureau of Labor Statistics, average annual inflation has hovered around 2–3% over the long term.

Together, these forces answer a practical question: should you take money now or later? In most cases, sooner wins—for growth, flexibility, and protection against rising prices.

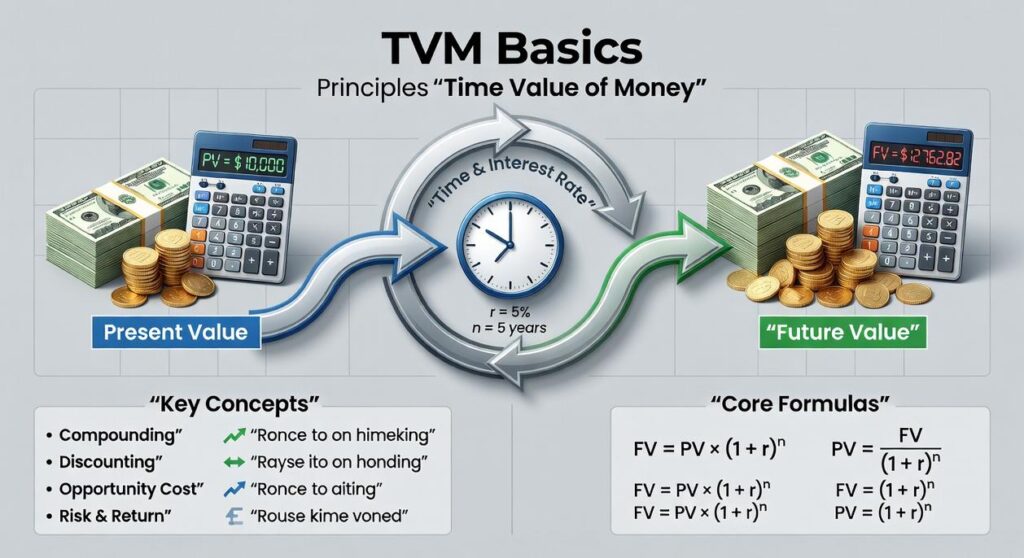

The Building Blocks of TVM: Decoding the Formula

At its core, the time value of money explained comes down to five building blocks. Think of them as the ingredients in a recipe—miss one, and the flavor changes completely.

Present Value (PV) is the current worth of a future sum of money. Imagine holding a crisp $100 bill today versus a promise of $100 five years from now. They may look identical on paper, but they don’t feel the same in your hand. PV asks: what is that future cash flow worth right now?

On the flip side, Future Value (FV) measures what today’s money could grow into over time. It’s the number you picture when planning retirement—the balance glowing on a screen decades from now. Some argue projections are guesswork. Fair point. Yet without estimating FV, goal-setting is like driving at night without headlights.

Then there’s the Interest Rate (i or r)—the engine under the hood. It’s either your reward for investing or the cost of borrowing. Even a small rate change can hum softly or roar loudly through your returns. Understanding how interest rates influence business financing decisions is essential (https://onpresscapital.com.co/how-interest-rates-influence-business-financing-decisions/).

Next, Number of Periods (n or t) refers to how often compounding happens. More periods mean more momentum—like a snowball gaining weight and speed downhill.

Finally, Payments (PMT) represent equal, recurring contributions or withdrawals. Think mortgage payments or monthly investments—the steady rhythm that shapes long-term outcomes.

TVM in the Real World: From Lottery Winnings to Retirement Savings

Understanding how money grows (or shrinks) over time isn’t just finance theory—it’s practical power. Once you see how it works, you start spotting smarter choices everywhere.

-

The Lottery Payout

Imagine winning $1 million paid over 20 years. The “lump sum” option might only be around $650,000–$750,000. Why? Because that lump sum represents the present value of all those future payments discounted at an assumed interest rate. In simple terms, if you invested the smaller amount today, it could grow to equal the total of those scheduled payments. That’s the time value of money explained in action: a dollar today is worth more than a dollar tomorrow because it can earn returns. The benefit? You can evaluate flashy offers with clear eyes instead of gut reactions. -

Your Savings Goal

Suppose you invest $5,000 today at 6% annually for 10 years. Using the future value formula:

$5,000 × (1.06)^10 ≈ $8,954. That’s nearly $4,000 in growth just from compounding. Compounding means earning returns on both your original money and prior interest (like a snowball picking up more snow). The upside for you: patience turns modest savings into meaningful wealth. -

Understanding a Loan

A car loan flips the equation. The loan amount is the present value, and your monthly payments repay it with interest over time. Lenders price loans using discounting math. Knowing this helps you compare rates confidently and potentially save thousands.

Master these principles, and everyday money decisions start working for you—not against you.

Putting TVM to Work: A Foundation for Wealth Growth

First, consider investment decisions. “I only buy when the discounted cash flows exceed today’s price,” one portfolio manager told me. That’s time value of money explained in action—discounting future cash flows to judge whether a stock or bond is worth buying now (a bit like deciding if a sequel is worth opening night prices).

Next, retirement planning becomes the ultimate TVM challenge. “How much do I need to save today?” a client asked. The math answers.

Finally, businesses rely on TVM daily, evaluating projects, machinery, and opportunities before committing capital.

Making Time Your Most Valuable Financial Asset

Have you ever wondered why two people investing the same amount end up with wildly different results? The answer, more often than not, is timing. As you’ve seen in the time value of money explained, a dollar today can grow—while a dollar tomorrow plays catch-up. Ignore that, and you’re quietly leaving money on the table.

So what happens if you start now instead of “next year”? Even modest, consistent investments can snowball through compounding (interest earning interest—yes, it’s that powerful). Try a simple calculator like this one: https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator and see for yourself. The earlier you begin, the harder your money works.

Turn Insight Into Action and Make Your Money Work Smarter

You came here looking for clarity on how money grows, why timing matters, and how smarter capital allocation builds long-term wealth. Now you have a clearer understanding of innovation trends, capital finance fundamentals, and the time value of money explained in practical terms you can actually use.

The real pain point isn’t lack of opportunity — it’s wasted time, missed compounding, and portfolios that drift without direction. Every year you delay optimizing your strategy is potential growth you don’t get back.

The next move is simple: review your current portfolio, identify underperforming assets, and apply these capital allocation principles immediately. Put your cash to work with intention, align it with long-term growth vehicles, and track performance consistently.

If you’re serious about accelerating wealth growth and eliminating guesswork, tap into expert-backed insights trusted by thousands of growth-focused investors. Get the strategies, alerts, and portfolio hacks you need to stay ahead — and start making every dollar count today.

Head of Financial Content & Portfolio Advisory

There is a specific skill involved in explaining something clearly — one that is completely separate from actually knowing the subject. Jeanda Larsonior has both. They has spent years working with wealth growth perspectives in a hands-on capacity, and an equal amount of time figuring out how to translate that experience into writing that people with different backgrounds can actually absorb and use.

Jeanda tends to approach complex subjects — Wealth Growth Perspectives, Portfolio Management Hacks, Innovation Alerts being good examples — by starting with what the reader already knows, then building outward from there rather than dropping them in the deep end. It sounds like a small thing. In practice it makes a significant difference in whether someone finishes the article or abandons it halfway through. They is also good at knowing when to stop — a surprisingly underrated skill. Some writers bury useful information under so many caveats and qualifications that the point disappears. Jeanda knows where the point is and gets there without too many detours.

The practical effect of all this is that people who read Jeanda's work tend to come away actually capable of doing something with it. Not just vaguely informed — actually capable. For a writer working in wealth growth perspectives, that is probably the best possible outcome, and it's the standard Jeanda holds they's own work to.

Head of Financial Content & Portfolio Advisory

There is a specific skill involved in explaining something clearly — one that is completely separate from actually knowing the subject. Jeanda Larsonior has both. They has spent years working with wealth growth perspectives in a hands-on capacity, and an equal amount of time figuring out how to translate that experience into writing that people with different backgrounds can actually absorb and use.

Jeanda tends to approach complex subjects — Wealth Growth Perspectives, Portfolio Management Hacks, Innovation Alerts being good examples — by starting with what the reader already knows, then building outward from there rather than dropping them in the deep end. It sounds like a small thing. In practice it makes a significant difference in whether someone finishes the article or abandons it halfway through. They is also good at knowing when to stop — a surprisingly underrated skill. Some writers bury useful information under so many caveats and qualifications that the point disappears. Jeanda knows where the point is and gets there without too many detours.

The practical effect of all this is that people who read Jeanda's work tend to come away actually capable of doing something with it. Not just vaguely informed — actually capable. For a writer working in wealth growth perspectives, that is probably the best possible outcome, and it's the standard Jeanda holds they's own work to.